Being behind on your mortgage is stressful. If you’ve fallen behind on your mortgage repayments and the pressure is building, it’s important to understand where you stand, and what you can do next to regain control. This guide explains what mortgage arrears means in a New Zealand context, how lenders typically respond, and the practical options that may be available. It is designed for borrowers who are already behind on their mortgage repayments and need to understand what happens next and what options may still be available.

Worried your mortgage arrears are getting worse?

If you are behind on payments or worried the situation may escalate, Platinum Mortgages can help you understand what options may still be available.

Mortgage arrears generally means there is an overdue amount on your home loan. In practice, many lenders may treat a loan as being in arrears from the first missed or overdue repayment, even if the situation has only just started.

If you’ve missed a single payment, learn what to do first in our missed mortgage payment article.

Arrears rarely happen overnight. More often, they build gradually as several pressures combine and make repayments harder to maintain over time. The most common causes include:

If any of these sound familiar, you’re not alone, and you’re not without options.

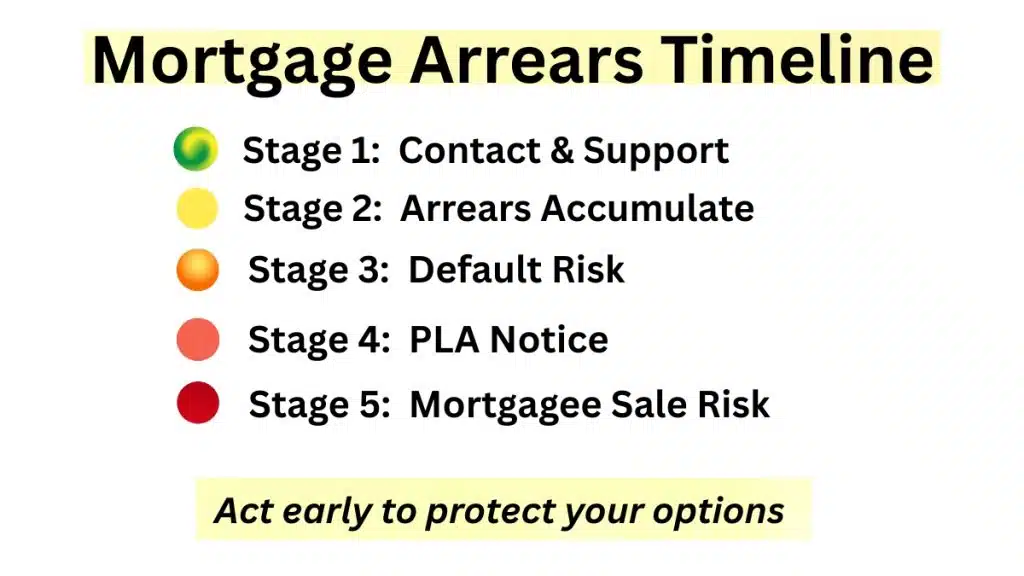

Once you’re in arrears, New Zealand lenders typically follow a structured process. Understanding this timeline matters, because each stage can reduce your available options if nothing changes.

Your lender will usually contact you to understand your situation and discuss next steps. Many lenders have hardship or support processes for borrowers experiencing financial difficulty, and this is often the stage where the most flexibility exists.

Missed payments are added to your outstanding loan balance. The debt grows, and the gap between where you are and where you need to be widens. Financial pressure at this stage tends to compound quickly.

If the situation continues without resolution, your lender may formally declare the loan in default. This is a significant legal step with lasting consequences for your credit file and borrowing future.

Before a mortgagee sale can proceed, the lender must issue a Property Law Act 2007 section 119 notice (PLA notice), with a minimum of 20 working days for the borrower to remedy the default.

Where arrears continue without resolution, the situation can escalate further. The lender may begin steps to sell the property to recover the debt. This is an outcome borrowers naturally want to avoid, and acting early may help preserve more options. If your situation has already reached default or mortgagee sale risk, our guide to what a mortgagee sale is in New Zealand explains what may happen next and why urgent advice matters.

These two terms are often used interchangeably, but they mean different things:

Arrears can lead to default, but that progression is not inevitable. Early action is often what prevents the situation from escalating further.

The key is acting early, before your options become limited. In our experience, borrowers who act early often have more options available than they expect:

This is the most immediate step and often more productive than many borrowers expect. In some situations, borrowers may be able to apply for hardship relief or discuss temporary changes to their repayments.

This conversation can feel uncomfortable, but lenders generally prefer a workable solution over the cost and complexity of enforcement.

If your current loan structure is the problem, refinancing could be the solution. Done well, refinancing can:

Learn more about refinancing your mortgage in New Zealand.

If credit cards, personal loans, or hire purchase agreements are eating into your cashflow and making your mortgage harder to service, consolidating those debts into your home loan could provide meaningful relief. It’s not the right fit for every situation, but in the right circumstances it can make a genuine difference to your monthly bottom line.

See how debt consolidation works.

If your bank is not willing or able to offer a workable solution, it is worth speaking with a mortgage adviser before the situation escalates further. In some cases, there may still be options to restructure, refinance, consolidate debt, or work through a specialist pathway, but the right approach depends on your equity position, repayment history, income, and how far the arrears have progressed.

In our experience, borrowers usually have more options when they seek help before arrears become entrenched.

You should act quickly if:

The longer arrears continue, the fewer options tend to remain. Acting early does not mean you have run out of options. It often means you still have time to put the right structure in place before the situation escalates further.

Mortgagee sale is not the usual first step when someone falls behind on their mortgage, but it can become a risk if arrears continue without a workable solution. The earlier you act, the more options you are likely to have before the situation reaches a formal enforcement stage.

If you are already receiving formal notices, or you believe your lender may be moving toward mortgagee sale, it is important to get advice quickly. At that point, the focus usually shifts from general arrears management to urgent steps to protect the property, review refinancing or restructuring options, and understand what can realistically be done before the situation escalates further.

If your situation has already reached default or mortgagee sale risk, our guide to what a mortgagee sale is in New Zealand explains what may happen next and what urgent steps may still be worth considering.

A broker works across the full lending market, not just with your existing bank. In an arrears situation, that breadth of access can be significant. A broker can:

Think of it as having an adviser in your corner – someone who understands what is negotiable, what is realistic, and how to present your situation clearly to lenders.

If you are already in mortgage arrears, putting the issue off usually makes the situation harder to solve. Reaching out can feel uncomfortable when money is already tight, but borrowers often have more options than they realise. The earlier those options are explored, the better the chances of finding a workable path forward.

Speak to a mortgage adviser today.

Angela is an accredited Financial Adviser, licensed under FSP742251 and has been in the Financial Industry since 2006. Our 5-star Google reviews reflect the excellent customer experience we promise — making your home loan journey positive, stress-free, and rewarding. At Platinum Mortgages, our clients are the reason we exist — so you can be confident every step is guided by genuine care and expertise.